Will Santa Bring Coal To Traders This Season?

It's been a while since our last post, so I'm not going to go into great detail about all the economic numbers reported since early November. Suffice it to say that the inflation reports released before Thanksgiving were better than most expected and certainly good news for inflation watchers. I've created a link to the releases for both the PPI and the CPI if you want detail.

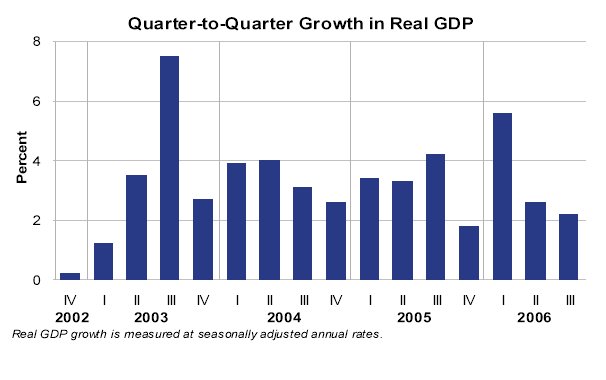

Yesterday (11/29/06) we got the first revision of 3rd quarter GDP. (There's one more revision on the way. Imagine trying to tell your boss you needed three tries to get your work right and keeping your job!) GDP was revised up to +2.2% versus the initial report of +1.6%. While it's clearly an improvement, 2.2% still represents a deceleration from the prior quarter. There was some good news on inflation in the report as core personal-consumption expenditure index rose 2.2% (yr./yr.) - down significantly from last quarter's 2.7% rise. This inflation number may still be high for some but at least it's heading in the right direction. And there was some impressive results on the corporate profit front with the government's number showing a 30% gain versus last year. Here's the link if you need all the gory details: Q3 GDP

initial report of +1.6%. While it's clearly an improvement, 2.2% still represents a deceleration from the prior quarter. There was some good news on inflation in the report as core personal-consumption expenditure index rose 2.2% (yr./yr.) - down significantly from last quarter's 2.7% rise. This inflation number may still be high for some but at least it's heading in the right direction. And there was some impressive results on the corporate profit front with the government's number showing a 30% gain versus last year. Here's the link if you need all the gory details: Q3 GDP

Of course, all these numbers are measures of historical performance. And as investors, we're more interested in what happens next. We've seen a few numbers (Chicago PMI, new unemployment claims, and some of the housing stats, for example) that make us think that economic growth will remain subdued going forward. It's probably not a great environment to sustain the high profit growth we've seen recently but it's a good bet interest rates stay in their current range. So right now we're looking for some appreciation in stocks next year - just nothing out of the ordinary.

And what about a Santa Claus rally this December? With some of the market averages already up double digits, we somewhat concerned that Santa will have coal in his bag.

Yesterday (11/29/06) we got the first revision of 3rd quarter GDP. (There's one more revision on the way. Imagine trying to tell your boss you needed three tries to get your work right and keeping your job!) GDP was revised up to +2.2% versus the

initial report of +1.6%. While it's clearly an improvement, 2.2% still represents a deceleration from the prior quarter. There was some good news on inflation in the report as core personal-consumption expenditure index rose 2.2% (yr./yr.) - down significantly from last quarter's 2.7% rise. This inflation number may still be high for some but at least it's heading in the right direction. And there was some impressive results on the corporate profit front with the government's number showing a 30% gain versus last year. Here's the link if you need all the gory details: Q3 GDP

initial report of +1.6%. While it's clearly an improvement, 2.2% still represents a deceleration from the prior quarter. There was some good news on inflation in the report as core personal-consumption expenditure index rose 2.2% (yr./yr.) - down significantly from last quarter's 2.7% rise. This inflation number may still be high for some but at least it's heading in the right direction. And there was some impressive results on the corporate profit front with the government's number showing a 30% gain versus last year. Here's the link if you need all the gory details: Q3 GDPOf course, all these numbers are measures of historical performance. And as investors, we're more interested in what happens next. We've seen a few numbers (Chicago PMI, new unemployment claims, and some of the housing stats, for example) that make us think that economic growth will remain subdued going forward. It's probably not a great environment to sustain the high profit growth we've seen recently but it's a good bet interest rates stay in their current range. So right now we're looking for some appreciation in stocks next year - just nothing out of the ordinary.

And what about a Santa Claus rally this December? With some of the market averages already up double digits, we somewhat concerned that Santa will have coal in his bag.

Labels: forecast, GDP, growth, inflation, stock market

posted by Under A Buttonwood Tree at 11:47 AM

0 comments

![]()

![]()